Strategic Tax Planning

for Entrepreneurs

How Billionaires Legally Minimize Their Taxes (And How Entrepreneurs Can Too)

What Is Strategic Tax Planning for Entrepreneurs?

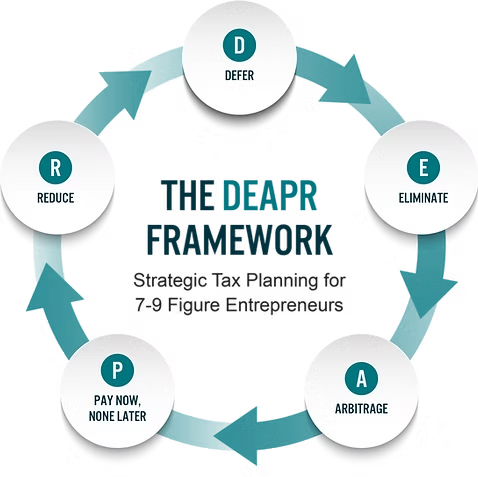

Strategic tax planning is the year-round practice of structuring your income, entities, and investments so you pay no more tax than the law requires—before the tax year closes, not after. It differs from tax preparation, which reports what already happened. Our Fractional Family Office® applies the proactive approach billionaire family offices use, organized around a five-part framework we call DEAPR: Defer, Eliminate, Arbitrage, Pay Now–None Later, and Reduce.

Based on data from hundreds of entrepreneur clients, our systematic tax planning process has generated significant tax savings, with a statistical average of $203,769 from 2024’s projections. Individual results vary considerably based on specific circumstances—see the disclosure at the bottom of this page.

Planning note for 2026: the One Big Beautiful Bill Act (signed July 4, 2025) rewrote several core entrepreneur strategies—100% bonus depreciation is back permanently, Section 179 doubled to $2.5 million, the QSBS exclusion grew to $15 million for newly issued stock, the SALT cap rose to $40,000 with a high-income phase-down, and the 20% pass-through deduction is now permanent. If your tax plan hasn’t been re-run since mid-2025, it’s running on the old code.

Tax is also only one lever in the bigger profit picture—our Profit Amplification framework shows how entrepreneurs increase profit margin across every line of the P&L.

And because taxes and portfolios interact at every step, the same proactive coordination extends to your family office investment strategy.

Who keeps all of these levers pulling in the same direction? That is the role of the Linchpin Partner®—your personal CFO.

And the wealth those strategies create needs defending—asset protection planning layers insurance, entities, and trusts so a lawsuit can’t take what tax planning saved.

Selling the company is the largest tax event of all—business exit planning aligns entity structure, QSBS, and deal timing years before the sale.

The Systematic Approach Behind the Savings

Our systematic tax planning process has helped entrepreneurs save between $0 and $904,313, with an average of approximately $203,769 in projected taxes based on 2024 data. Every situation is unique, and results vary significantly with individual income and circumstances.

How do we pursue those results? Through a systematic four-phase process that transforms reactive tax compliance into proactive tax strategy:

Phase 1: Deep Historical Analysis

We begin by analyzing past tax returns to uncover missed opportunities and savings potential:

- Comprehensive review of past 2 years of tax returns (personal and business)

- Identification of missed opportunities

- Analysis of current tax burden across all entities and jurisdictions

- Documentation of specific potential savings areas with projected impact

- Detailed tax situation benchmarking against similar businesses

During this phase, we often find entrepreneurs have been missing key strategies for years. Sometimes we find basic errors and can amend prior returns—which can mean immediate refunds from the IRS.

Phase 2: Strategic Development Using the DEAPR Framework

We leverage our proprietary DEAPR Framework to create a customized tax strategy that optimizes every aspect of your tax situation. DEAPR stands for:

- Defer: Make Uncle Sam Wait

- Eliminate: Make Taxes Disappear (Legally)

- Arbitrage: Play Different Tax Rates Against Each Other

- Pay Now, None Later: Front-Load Tax for Future Freedom

- Reduce: Maximize Deductions and Credits

Defer: Make Uncle Sam Wait

Tax deferral follows a simple principle: a dollar in your pocket today is worth more than a dollar in your pocket tomorrow. When you defer taxes, you're not just saving on today's tax bill—you're allowing your money to compound without the drag of taxation. Key strategies include:

Eliminate: Make Taxes Disappear (Legally)

While deferral is powerful, elimination is the holy grail of tax planning. These strategies can permanently remove tax liability—not just postpone it. Key elimination strategies include:

Arbitrage: Play Different Tax Rates Against Each Other

Tax arbitrage involves leveraging differences in tax rates across time periods, entities, income types, or family members to reduce your overall tax burden. This sophisticated approach exploits legitimate rate disparities built into the tax code. Key arbitrage strategies include:

Pay Now, None Later: Front-Loading Tax for Future Freedom

Sometimes the smartest tax move isn't to minimize your current tax bill—it's to pay taxes strategically now to eliminate them completely in the future. This approach requires long-term thinking and disciplined planning. Key "Pay Now, None Later" strategies include:

Reduce: Maximize Deductions & Credits

Reduction strategies focus on decreasing your taxable income through deductions, exclusions, and credits—areas where most entrepreneurs leave significant money on the table. Key reduction strategies include:

Phase 3: Implementation & Coordination

Unlike most tax advisors who simply make recommendations and leave you to figure out the details, we take a hands-on approach to implementation:

- Coordinate with your existing tax team to ensure seamless execution

- Create detailed implementation timelines and action plans for each strategy

- Model different scenarios to quantify potential ROI before implementation

- Manage documentation and compliance requirements that support audit readiness

- Oversee implementation across all entities and tax jurisdictions

- Provide ongoing support throughout the implementation process

Phase 4: Ongoing Optimization

Tax strategy isn't a one-time event—it's an ongoing process that requires constant monitoring and adjustment:

- Quarterly strategy reviews to identify new opportunities and adjust existing strategies

- Proactive planning for major events like business acquisitions, sales, or real estate transactions

- Regular coordination with your tax preparation team to ensure alignment

- Continuous identification of new opportunities as tax laws change

- Annual strategy refresh to incorporate changes in your business and personal situation

Our month-by-month tax planning checklist sets out what each quarter of the year requires, with the 2026 filing and election deadlines attached.

"Not only did I pay zero federal income taxes last year for all of my companies, I got money back, and he got me $3.5 million in carryforward for the coming year."

Pace Morby

Unpaid client testimonial

Individual results vary. This testimonial may not be representative of other clients’ experiences and is no guarantee of future results.

Our DEAPR Framework in Action

While every entrepreneur’s situation is unique, here are examples of how we systematically implement tax-saving strategies across various levels of complexity:

Foundation Strategies

The Augusta Rule (Section 280A), Properly Documented

- Rent your personal residence to your business up to 14 days annually for legitimate business use

- Tax-free income to you, deductible to the company—at documented fair-market venue rates

- Built to the documentation standard the Tax Court applied in Sinopoli v. Commissioner

- Systematic documentation and implementation process

Strategic Entity Design for 199A Optimization

- Restructure business entities to protect the 20% qualified business income deduction—now permanent

- Strategic wage and profit allocation modeling

- Potential to save thousands (or hundreds of thousands) annually through proper structuring

Advanced Exit Architectures

Dynasty Trust & Section 1202 Integration

- Strategic use of dynasty trusts to multiply Section 1202 qualified small business stock exclusions

- Potential for tens of millions in tax-free proceeds from right-fit business sales

- Multi-generational tax benefits, designed with estate counsel as part of your wealth transfer planning

Section 1202 is one lever among several at exit. Our deep dive on selling a business tax strategies sets out the installment, charitable, ESOP and opportunity-zone alternatives alongside it, and the deadline each one carries.

“Dew was instrumental in guiding myself and my partners with tax and asset protection through this process. Working with Jim and his team for two decades has been one of the smartest decisions I have made for myself and my family.”

Brad Baumgardner, founding partner of Interior Logic Group, which sold to Blackstone for $1.6B in 2021

Unpaid client testimonial

Individual results vary. This testimonial may not be representative of other clients’ experiences and is no guarantee of future results.

.avif)

"They were able to put in tax strategies to save me hundreds of thousands of dollars. I highly recommend Jim Dew and Dew Wealth and the virtual family office. Take it from a high-net-worth individual who's gotten massive value."

Joel Marion, Co-Founder of BioTrust Nutrition

Unpaid client testimonial

Individual results vary. This testimonial may not be representative of other clients’ experiences and is no guarantee of future results.

Taking the Next Step

If you're an entrepreneur generating $1M+ in annual revenue and want to explore how our systematic approach to tax planning could benefit your situation, let's talk. Schedule a strategy call with us to review your tax opportunities.

During this call, we'll:

Review Your Current Tax Situation

Identify Potential Opportunities

Explain Our Systematic Approach