The Entrepreneur's

Guide to Wealth Transfer Planning

Protecting Your Legacy and Values Beyond Basic Estate Planning

Wealth transfer planning is the process of passing your wealth—and the values that built it—to the people and causes you choose, with minimal taxes, delay, and family conflict. For entrepreneurs, it goes beyond basic estate planning: your business is often your largest asset, and roughly 70% of family wealth transfers fail by the third generation, according to Williams and Preisser's study of 3,250 families. This guide covers the legal foundations, the 2026 federal estate tax rules, and the strategies entrepreneurs use to address the causes behind that failure rate.

As a successful entrepreneur, you've spent years—perhaps decades—building your business and wealth from the ground up. But have you considered what happens to everything you've built when you're no longer at the helm? While you've mastered business strategy, scaling operations, and capital allocation, the ultimate exit strategy—what happens to your wealth and business when you're gone—often remains neglected.

This isn't just about documents and taxes. It's about ensuring your life's work continues to make an impact according to your vision, values, and intentions. Whether you're just crossing into seven-figure territory or managing a nine-figure enterprise, the time to think about wealth transfer is now—before circumstances force decisions out of your control.

Schedule a Confidential Wealth Transfer Strategy Session

Cornelius Vanderbilt

Why Do 70% of Wealth Transfers Fail?

The 70% Failure Rate

Here's a statistic that should concern every successful entrepreneur: roughly 70% of wealth transfers fail. In a study of 3,250 families conducted over about two decades and published as Preparing Heirs, Roy Williams and Vic Preisser measured how often family wealth survives its own transition. The Institute for Preparing Heirs, the organization that carries that research forward, states the finding as 70% of unprepared families losing control of their assets and their family unity by the third generation.

This isn't primarily due to poor investment decisions or economic downturns. The same research attributes the failures as follows:

- 60% — a breakdown of trust and communication within the family

- 20% — heirs left unprepared for the responsibility

- 15% — the absence of a shared family mission

- Less than 5% — errors in the estate documents themselves

Those shares are the study's own attribution across its sample, not a prediction for any particular family.

These “soft” factors—not estate taxes, and not the drafting—are what most often destroy generational wealth. Consider the Vanderbilt family. Cornelius Vanderbilt amassed the largest American fortune of his era—roughly $105 million at his death in 1877, more than the U.S. Treasury held at the time. Yet when 120 of his descendants gathered for a family reunion at Vanderbilt University in 1973, family historian Arthur T. Vanderbilt II records in Fortune's Children that not a single millionaire remained among them. The fortune had evaporated within three generations.

Warren Buffett

The Cost of Doing Nothing

Avoiding wealth transfer planning doesn't mean avoiding the consequences—it means surrendering control over them. Without proper planning, you face:

- Probate court deciding how to distribute your assets

- Potential business disruption or forced liquidation

- Family conflict over business control and inheritance

- Up to 40% of your wealth being consumed by estate taxes

- Your values and vision disappearing with you

As Warren Buffett told Fortune back in 1986, the right amount to leave your children is "enough money so that they would feel they could do anything, but not so much that they could do nothing."

Essential Legal Foundations

Every entrepreneur's wealth transfer plan starts with four core documents: a last will and testament, financial and healthcare powers of attorney, healthcare directives, and—for most business owners—a revocable living trust. Together they form the estate planning framework that protects your assets and ensures your basic wishes are followed.

Last Will & Testament

A will is the starting point for any estate plan, specifying:

- Who receives your assets

- Who will care for minor children

- Who will execute your estate

Entrepreneur Alert: A basic will alone is insufficient for most 7-9 figure entrepreneurs. It becomes public record during probate, provides minimal protection against taxes, and offers limited control over how assets are used after your death.

Power of Attorney

This document designates who will make decisions if you become incapacitated—a possibility that entrepreneurs often overlook despite its devastating potential impact on their business.

Financial Power of Attorney

Ensures business operations continue uninterrupted if you're temporarily unable to manage them

Healthcare Power of Attorney

Designates a trusted person to make medical decisions on your behalf if you become unable to do so

Revocable Living Trusts

For entrepreneurs with complex business interests, a revocable living trust maintains business continuity during incapacity and after death, and offers significant advantages over a will alone:

Avoiding

Probate

Keeping your Affairs Private & Reducing Delays

Providing for

Incapacity

Ensuring Seamless Management of your Assets

Offering More

Control

Over How and When Beneficiaries Receive Assets

Creating

Flexibility

For Changes as Your Circumstances Evolve

What Is a Family

Mission Statement?

A family mission statement is a short written document that captures the values behind your wealth so they can guide the generations who inherit it. It serves as an ethical constitution for your family, providing clarity and continuity of purpose long after you're gone.

A family mission statement articulates:

- Core values that guided your wealth creation

- Vision for the future of your family and business

- Principles for decision-making across generations

- Expectations for wealth stewardship

The Rockefeller family exemplifies this approach. John D. Rockefeller established clear family values centered on philanthropy, stewardship, and education. Now in its seventh generation, the family still gathers regularly—often more than 100 members at a time—to discuss those values and how to apply them in contemporary contexts (CNBC, 2018). Their wealth has endured not just because of sophisticated financial structures, but because of a shared mission that transcends the founder.

A mission statement is the shortest of the governance documents. Turning it into a working system, with a family council, a meeting calendar and written decision rights, is the subject of our guide to family governance.

Sam Walton

Billionaire Strategies for Dynastic Wealth

The ultra-wealthy don't simply accept estate taxation as inevitable—they implement sophisticated strategies to minimize or even eliminate it. When properly executed, these same approaches are available to seven and eight-figure entrepreneurs as well. These are complex vehicles: suitability depends on your circumstances, and experienced legal and tax counsel is essential.

How Does a GRAT Work? The Walton Family Approach

A Grantor Retained Annuity Trust (GRAT) lets you transfer an asset's future appreciation to your heirs with little or no gift tax. The strategy gained fame through the Walton family: Audrey Walton's 1993 GRATs led to a 2000 Tax Court decision that legitimized the "zeroed-out" GRAT, and Bloomberg-analyzed filings later showed the family moving more than $9 billion in Walmart shares to heirs through 57 GRATs between 2007 and 2016.

Here's how it works:

- Assets are placed in a trust for a specific term (typically 2-10 years)

- The grantor receives annuity payments during the term

- At the end of the term, remaining assets pass to beneficiaries

- The gift tax is calculated only on the projected remainder value at inception

The advantage comes when assets appreciate faster than the IRS-assumed rate of return (the Section 7520 "hurdle rate"). That excess appreciation passes to heirs free of gift and estate taxes. For entrepreneurs with high-growth businesses or investments, GRATs offer a way to transfer future appreciation without transfer-tax consequences—though if the assets underperform or the grantor dies during the term, the expected benefit can be lost.

Mark Zuckerberg

Mark Zuckerberg

IDGTs: The Silent Wealth Transfer Vehicle

The Intentionally Defective Grantor Trust (IDGT) is another powerful tool for transferring business interests or appreciating assets to the next generation:

- The trust is "defective" for income tax purposes but effective for estate tax purposes

- The grantor pays income taxes on trust earnings, effectively gifting beneficiaries tax-free

- Assets sold to the trust can be transferred with minimal gift tax impact

- Future appreciation occurs outside the grantor's estate

For entrepreneurs selling their business or transferring ownership interests, IDGTs can shift substantial value to heirs while keeping income taxes simple. Mark Zuckerberg famously used a related technique—the zeroed-out GRAT—to transfer Facebook shares before the company's 2012 IPO; Forbes estimated the founders' GRATs moved more than $200 million free of gift tax. Like GRATs, IDGTs require experienced counsel to structure properly.

Dynasty Trusts: Multi-Generational Protection

Dynasty trusts represent the pinnacle of generational wealth planning, designed to last for multiple generations—potentially forever in some states:

- Assets placed in the trust remain outside the estate tax system for the trust's duration

- Each generation can benefit from the assets without owning them directly

- The trust provides protection against creditors, divorce, and poor financial decisions

- Wealth can compound for generations without estate tax erosion

South Dakota and Delaware have abolished the traditional "rule against perpetuities" that once limited trust duration, and Nevada allows trusts to run for up to 365 years. The Rockefeller family pioneered the multigenerational trust approach, with structures that have now benefited the family into its seventh generation while maintaining family control over assets.

Which Trust Strategy Fits Which Goal?

| Strategy | Best for | Key benefit | Typical horizon |

|---|---|---|---|

| GRAT | Rapidly appreciating assets (pre-sale or pre-IPO business interests) | Appreciation above the IRS hurdle rate passes free of gift and estate tax | 2–10 years |

| IDGT | Income-producing business interests sold or gifted to the trust | Grantor pays the trust's income taxes, letting assets compound for heirs outside the estate | Long-term |

| Dynasty trust | Multi-generational wealth preservation | Keeps assets outside the estate tax system for generations, with creditor and divorce protection | Generations—perpetual in some states |

.avif)

Strategic Philanthropy:

Leaving a Greater Legacy

For many entrepreneurs, building wealth isn't just about financial success—it's about making a meaningful impact on the world. Strategic philanthropy allows you to extend your values and vision beyond your lifetime while potentially providing significant tax benefits as part of comprehensive tax planning for business owners.

Donor-Advised Funds (DAFs)

A donor-advised fund gives you an immediate tax deduction while allowing you to recommend grants to charities over time:

- Immediate tax deduction for the full contribution

- No capital gains tax on appreciated assets donated

- Tax-free growth of the donated assets

- Simplified administration compared to private foundations

- Low or no minimums—the largest national sponsors have eliminated initial-contribution minimums entirely

Many entrepreneurs use DAFs as a stepping stone to more sophisticated charitable vehicles, establishing a family tradition of giving while minimizing tax burdens.

Charitable Remainder Trusts (CRTs)

A charitable remainder trust provides income to you or your beneficiaries for a term of years or lifetime, with the remainder going to charity:

- Immediate partial tax deduction based on the projected charitable remainder

- No capital gains tax when appreciated assets are sold within the trust

- Income stream for you or your beneficiaries

- Estate tax reduction for assets ultimately passing to charity

For entrepreneurs with highly appreciated assets (like business interests before a sale), CRTs can provide significant income while reducing tax burdens and supporting causes you care about.

Private Foundations

Private foundations offer maximum control over charitable giving and can become a vehicle for family values across generations:

- Complete control over grant-making decisions

- Ability to hire family members (with reasonable compensation)

- Public recognition of your philanthropic legacy

- Potential to continue for generations

- Minimum annual distribution requirement of 5% of assets (IRC Section 4942)

Bill Gates, MacKenzie Scott, Jeff Bezos, and Warren Buffett have all created major philanthropic vehicles—from the Gates Foundation to Yield Giving and the Bezos Earth Fund—to channel their wealth toward solving societal problems while building a legacy beyond their business achievements.

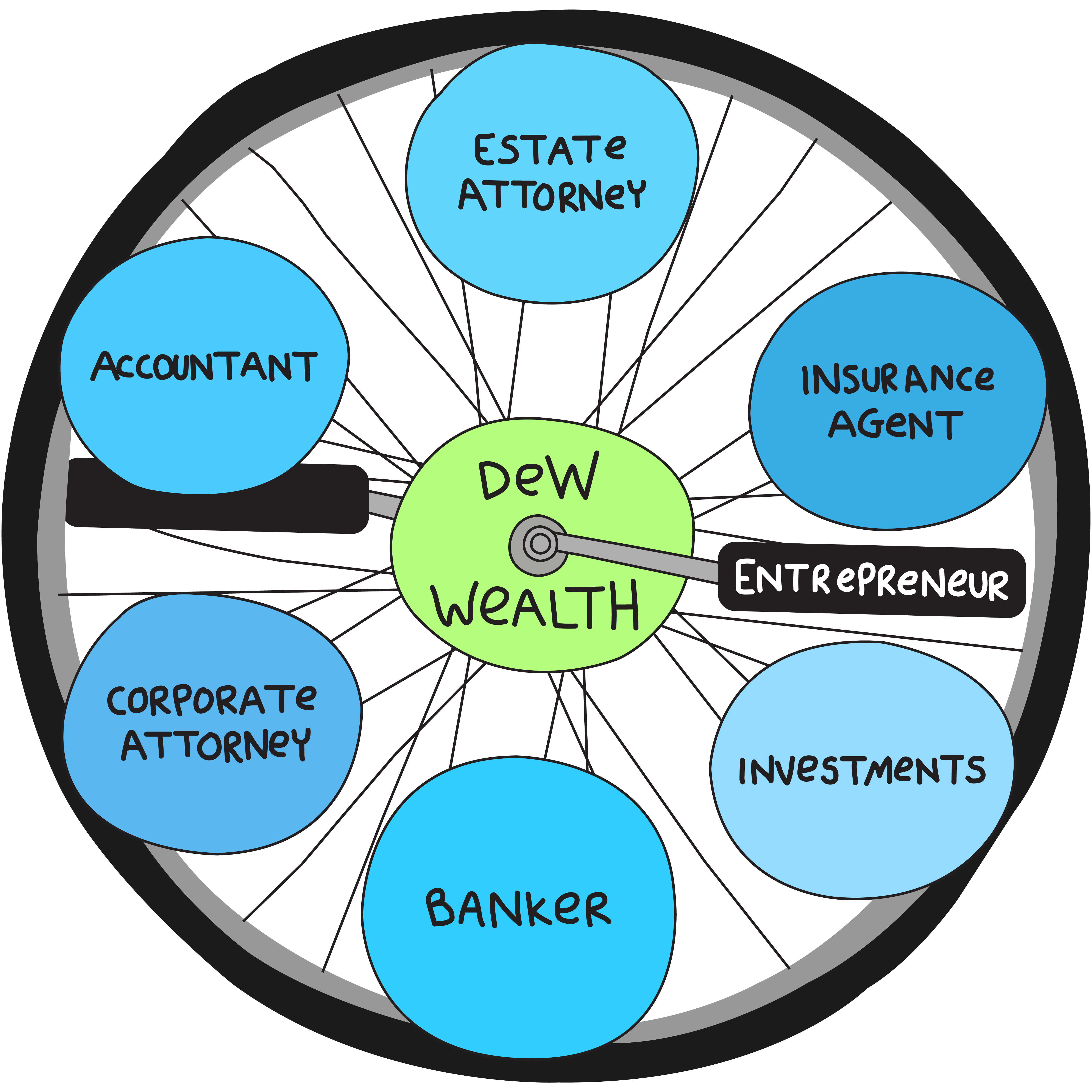

Who Should Be on Your Wealth Transfer Team?

Effective wealth transfer planning requires specialized expertise across multiple disciplines. For seven to nine-figure entrepreneurs, the right team spans six roles:

Your wealth transfer team should include:

- Estate Planning Attorney: Specializing in complex business successions and high-net-worth planning

- Wealth Manager: Experienced in entrepreneurial wealth, alternative investments, and family office investment strategy

- CPA: Focused on tax strategies for business owners and wealth transfer

- Business Valuation Expert: For accurate assessment of your most valuable asset

- Insurance Professional: To address liquidity needs for taxes and business continuity

- Trust Officer: For long-term trust administration and implementation

Coordinating these six specialists is itself a significant time commitment—which is why our approach to wealth management for business owners, the Time-Energy Shield, delegates that coordination to a single integrated team, led by your Linchpin Partner®—a personal CFO for your entire financial life.

Strengthening the business before a transition compounds that team's work—see how entrepreneurs increase their profit margin to raise both sale value and the wealth available to transfer.

Defending that wealth while it grows—and while it transfers—is the work of asset protection planning: insurance, entities, and trusts layered so lawsuits and creditors can’t undo the plan.

For owners, the largest transfer event is usually the sale of the company itself—business exit planning coordinates that transaction with the estate plan so value survives both the sale and the transfer.

Whether that sale happens at all is the prior question, and it decides which of these specialists you need first—business succession planning sets the family-transfer and external-sale paths side by side on value, tax, timing and control.

"Working with a coordinated wealth management team for two decades has been one of the smartest decisions I have made for myself and my family. They were instrumental in guiding myself and my partners with tax and asset protection through the process."

Brad Baumgardner, who sold his company to Blackstone in a $1.6 billion transaction

Unpaid client testimonial