Most entrepreneurs are flying blind on their own balance sheet, and the tool meant to prevent it is often the cause. Automated net worth trackers and account-aggregation feeds pull in balances instantly, but they routinely get ownership wrong, confusing which account belongs to you, your spouse, your trust, or your kids. If you can't explain every single line on your own balance sheet, verified against real statements, you don't actually know what you own.

What does "flying blind" on your own finances actually look like?

Picture a business owner and spouse with a rolled-up equity stake in a holding company, accounts scattered across several custodians, and a handful of alternative investments spread across different platforms. On paper, their net worth dashboard looks clean: every account pulled in, every balance current. In practice, when someone actually opened the real custodian statements and checked, the automated feed had the ownership wrong on nearly half the accounts, misattributing which entity, spouse, or trust actually held each one.

This is not a software bug. It is the default state of any balance sheet that has never been checked line by line against source documents, which describes most entrepreneurs' financial pictures once their affairs grow past a single brokerage account.

Why do net worth trackers and account-aggregation feeds get ownership wrong?

Automated feeds are built to do one thing reliably: pull a dollar balance from a linked account. They are not built to verify who legally owns that account. So they guess, usually based on whatever label was typed in when the account was first linked, sometimes years earlier and never revisited. A joint account can default to the wrong titling. A trust account can show up as an individual holding. A child's custodial account can quietly blend into a parent's total. The dollar figure is usually right. The ownership behind it frequently is not.

That distinction matters more as an entrepreneur's financial life gets more complex: multiple entities, multiple custodians, alternative investments, and family trusts all stacking on top of each other. The more moving pieces, the more a feed is guessing rather than verifying.

What does real financial mastery of your own balance sheet actually require?

The standard is simple to state and uncomfortable to apply: if you cannot explain every single line on your own balance sheet, verified against an actual statement, something is wrong. Either you do not fully know what you own, or the structure behind it was built without much care and has not been checked since. That is not a compliance exercise. It is the difference between believing you understand your financial position and actually understanding it.

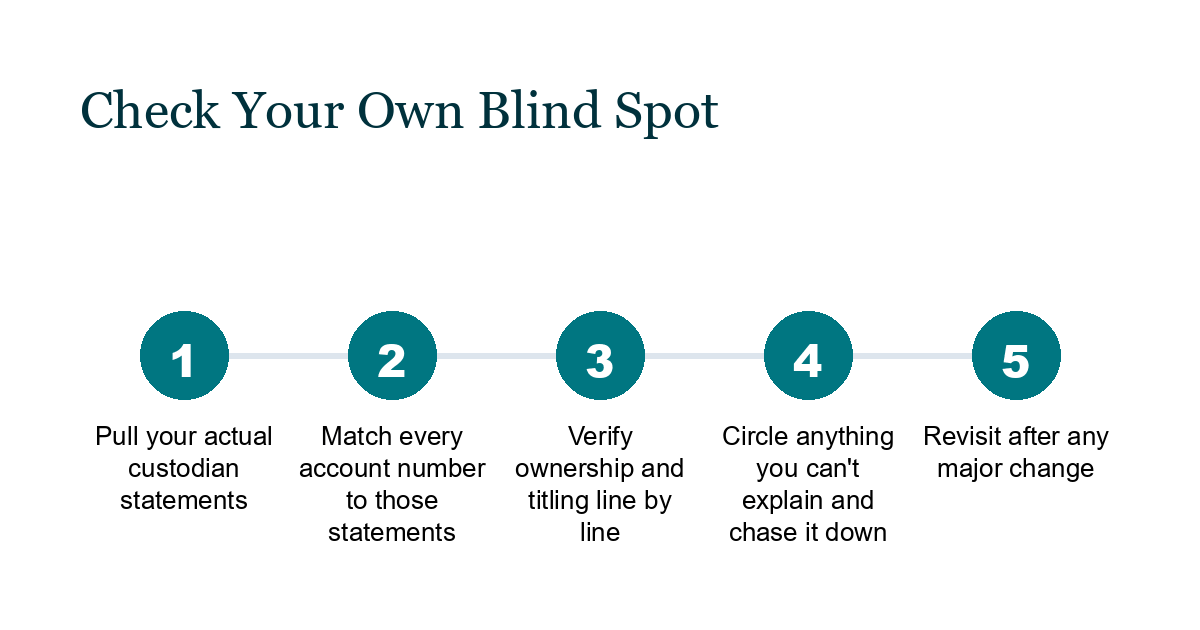

Getting there means going line by line: pulling the real statements from every custodian, matching account numbers by hand, and circling anything that cannot be explained until it can. Where accounts are jointly titled and the couple lives in a community-property state, simplifying that titling, with an attorney's guidance, removes one more source of confusion from the balance sheet going forward.

Why does an inaccurate balance sheet create real financial risk?

An incorrect balance sheet is not just messy paperwork. Estate documents get drafted against account ownership that turns out to be wrong. Insurance coverage gets sized against a net worth figure that double-counts or omits accounts. Tax planning gets built around whose name an asset sits in, and if that is wrong, so is the plan. None of these mistakes surface until the moment they matter most, a death, a lawsuit, a sale, or an audit, which is exactly when there is no time left to discover the balance sheet was never actually accurate.

How does one blind spot fit into the bigger wealth-wheel picture?

A balance sheet blind spot rarely shows up alone. It tends to appear alongside the broader pattern Dew Wealth calls the Financial Flat Tire: a capable accountant, attorney, insurance agent, and investment advisor, each doing solid work in their own lane, none of them coordinating with the others, leaving the entrepreneur stuck in the middle as the de facto project manager of their own financial life. An accurate, fully reconciled balance sheet is the starting point any coordinated plan has to stand on. Without it, every downstream decision, tax planning, investment allocation, estate strategy, is being made on numbers nobody has actually verified.

How can you check for this blind spot in your own finances?

The process does not require new software or a bigger dashboard. It requires going back to source documents and treating the exercise as non-negotiable.

Certain moments make this check especially urgent: rolling several entities into a new holding structure, adding a family trust, onboarding a new advisor or custodian, or preparing for a liquidity event. Any of these can introduce new accounts, new titling, or new intermediary entities faster than a dashboard can accurately reflect them. Do the exercise once, and it gets easier every year after, because accounts get correctly labeled and ownership gets documented instead of guessed. Trusting the dashboard indefinitely just lets the blind spot compound quietly in the background.

Where a coordinated financial team fits in

This is one of the reasons the Fractional Family Office® model exists: not to replace the discipline of checking your own numbers, but to put a coordinated team behind that discipline instead of leaving an entrepreneur to reconcile a fragmented balance sheet alone. Balancing every spoke of the wealth wheel, tax, investments, entity structure, insurance, and transfer planning, starts with a balance sheet everyone actually trusts.

See how the full framework fits together in Balancing Your Wealth Wheel, or get an overview of the model at the Fractional Family Office® hub.